大浩浩的笔记课堂——FRM考试学习笔记136

- 2026-04-13 23:35:44

Topic 65 Portfolio Risk:Analytical Methods

1.Portfolio VaR measures:

⑴portfolio VaR & individual VaR:

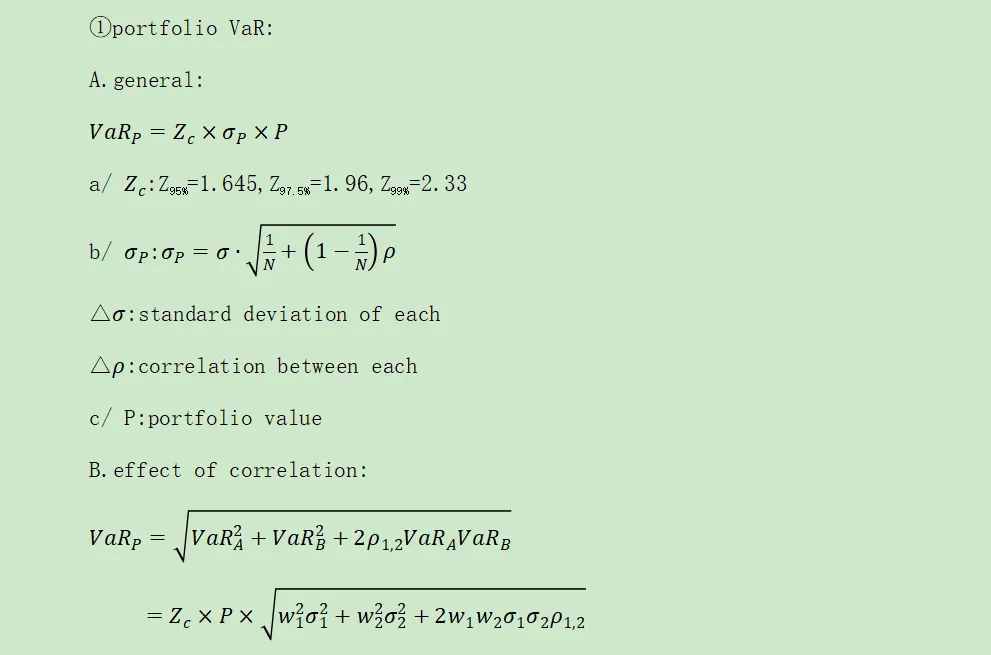

①portfolio VaR:

②individual VaR:

A.definition:

It is the VaR of an individual position in isolation.

B.formula:

⑵diversified VaR & undiversified VaR:

①diversified VaR:

A.definition:

Taking into account diversification benefits between components.

B.formula:

②undiversified VaR:

A.definition:

The portfolio VaR when there is no short position and all correlations are unity.

B.formula:

2.VaR tools(Other portfolio VaR measures):

⑴marginal VaR(Δ=1):

①definition:

It is the per dollar change in portfolio VaR that occurs from an additional investment in as position.

②formula:

③usage:

How to use it:

A.obtain the optimal portfolio:

Equating the excess return/MVaR ratio of all portfolio positions.

B.obtain the lowest portfolio VaR:

Equating just the MVaRs of all portfolio positions.

⑵incremental VaR(Δ=any $):

①definition:

It is a change in VaR from the addition of a new position in a portfolio.

②formula:

③characteristic:

A.It is the change in VaR owing to a new position.

B.It differs from the marginal VaR in that the amount added or subtracted can be large,in which case VaR changes in a nonlinear fashion.

C.Comparing to using marginal VaRs,computing with full revaluation is more costly,but also more accurate.

④usage:

It applies to the general case where a trade involves a set of new exposes on the risk factors.

⑤drawback:

It requires a full revaluation of the portfolio VaR with new trade.

⑥best hedge:

A.The best hedge is additional amount to invest in an asset so as to minimize the risk of the total portfolio.

B.less costly approximation method:

a/ Breaking down the new position into risk factors.

b/ Multiplying each new risk factor times the corresponding partial derivative of the portfolio with respect to factors.

c/ Adding up all the values.

⑶component VaR(Δ=pi):

①definition:

It is the amount of risk a particular fund contributes to a portfolio of funds.(not elliptical)

②formula:

③characteristic:

A partition of the portfolio VaR that indicates how much the portfolio VaR would change approximately if the given component was deleted by construction,component VaRs sum to the portfolio VaR.

3.Examples:

⑴A Global Portfolio Equity Report

⑵Barings:An Example in Risks

4.Managingportfoliosusing VaR:

⑴from risk measurement to risk management:

①changing:

A.Positions should be cut first where the marginal VaR is the greatest,keeping portfolio constraints satisfied.

B.With the lowest marginal VaR,it should be added to make up for the first charge.

②repeating:

Repeating process until reached a global minimum.

③verifying:

The betas of all positions are equal when risk is minimized.

·特别注意!

·for lowest portfolio VaR:

The MVaRs of all portfolio positions must be equal.

⑵from risk management to portfolio management:

for optimal portfolio(portfolio risk will be at a global minimum):

大浩浩的笔记课堂之FRM考试学习笔记合集

【正文内容】

FRM二级考试

A.Market Risk

A.市场风险

Topic 1 Estimating Market Risk Measures:An Introduction and Overview

Topic 2 Non-Parametric Approaches

Topic 3 Parametric Approaches:Extreme Value

Topic 6 Messages from the Academic Literature on Risk Management for the Trading Book

Topic 7 Some Correlation Basics:Properties,Motivation and Terminology

Topic 8 Empirical Properties of Correlation:How Do Correlation Behave in the Real World

Topic 9 Statistical Correlation Models—Can We Apply Them to Finance

Topic 10 Financial Correlation Modeling—Copula Correlations

Topic 11 Empirical Approaches to Risk Metrics and Hedging

Topic 12 The Science of Term Structure Models

Topic 13 The Shape of the Term Structure

Topic 14 The Art of Term Structure Models:Drift

Topic 15 The Art of Term Structure Models:Volatility and Distribution

Topic 16 Overnight Index Swap(OIS) Discounting

B.Credit Risk

B.信用风险

Topic 20 Default Risk:Quantitative Methodologies

Topic 21 Credit Risks and Credit Derivatives

Topic 22 Credit and Counterparty Risk

Topic 23 Spread Risk and Default Intensity Models

Topic 25 Structured Credit Risk

Topic 26 Defining Counterparty Credit Risk

Topic 27 The Evolution of Stress Testing Counterparty Exposures

Topic 28 Netting,Compression,Resets,and Termination Features

Topic 32 Default Probability,Credit Spreads and Credit Derivatives

Topic 33 Credit Value Adjustment(CVA)

Topic 35 Credit Scoring and Retail Credit Risk Management

Topic 38 Understanding the Securitization of Subprime Mortgage Credit

C.Operational Risk

C.操作风险

Topic 39 Principles for the Sound Management of Operational Risk

Topic 40 Enterprise Risk Management:Theory and Practice

Topic 41 Observations on Developments in Risk Appetite Frameworks and IT Infrastructure

Topic 42 Operational Risk Data and Governance

Topic 45 Validating Rating Models

Topic 47 Risk Capital Attribution and Risk-Adjusted Performance Measurement

Topic 48 Range of Practices and Issues in Economic Capital Framework

Topic 49 Capital Planning at Large Bank Holding Companies

Topic 50 Repurchase Agreements and Financing

Topic 51 Assessing the Quality of Risk Measures

Topic 52 Estimating Liquidity Risks

Topic 53 Liquidity and Leverage

Topic 54 The Failure Mechanics of Dealer Banks

Topic 56 Introduction of Basel Accord

Topic 58 Basel Ⅱ.5 and Fundamental Review of the Trading Book(FRTB)

D.Investment Risk

D.投资风险

Topic 62 Factors in Investment

Topic 63 The Low-Risk Anomaly and Alpha