大浩浩的笔记课堂——FRM考试学习笔记134

- 2026-04-16 21:59:07

Topic 63 The Low-Risk Anomaly and Alpha

1.Low-risk anomaly:

⑴definition:

It violates the CAPM and suggests that low beta stocks will outperform high-beta stocks.

⑵comparison:

Higher risk,as measured by beta,should have a higher return.But in the low-risk anomaly,firms with lower betas and lower volatility have higher returns over time.

⑶explanations:

①The potential explanations for the risk anomaly are:

data mining:

It is not well supported.

②investor constraints(leverage):

leverage constraints on retail investors(that drive them to buy pre-leveraged investment in the form of high-beta stocks)

③institutional manager constraints:

institutional investor constraints such as prohibitions against short selling or tracking error tolerance bands

④preference theory:

the preferences of investors

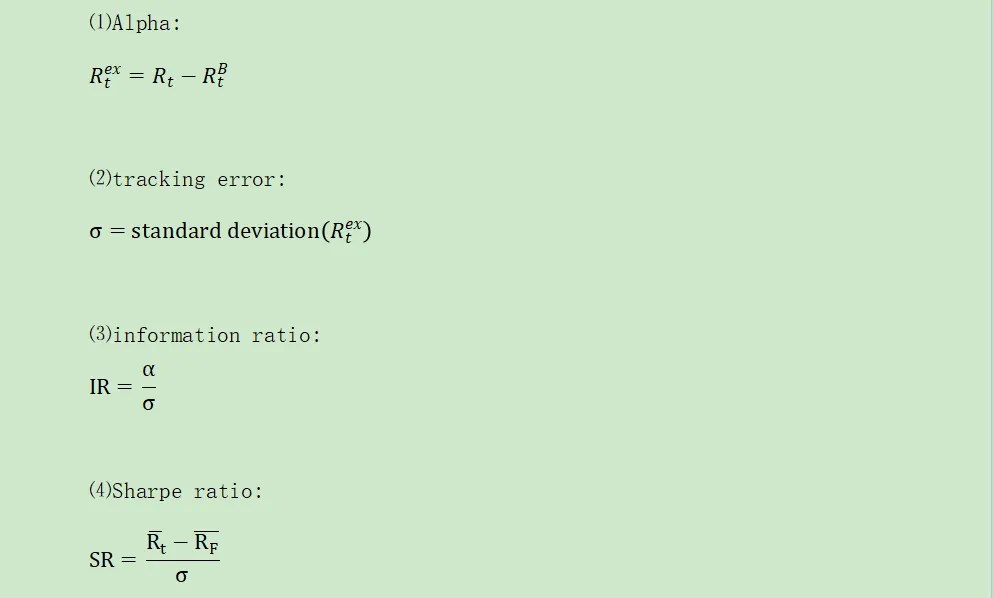

2.Formulas related to alpha:

3.Benchmark selection for alpha:

⑴If the benchmark is riskier than the investment in question,then both the alpha and the information ratio will be too low.

⑵The best combination for a benchmark is for it to be well-defined,tradable,replicable and adjusted for the risk of the underlying pool of investments.

4.Fundamental law of active management:

⑴formula:

A tradeoff between the number of investment bets placed(breath) and the required degree of forecasting accuracy(information coefficient):

⑵investor:

①place a large number of bets and not be very concerned with forecasting accuracy

②need to be very good at forecasting if he places only a small number of bets

5.Factors regression and portfolio sensitivity:

⑴models:

①traditional capital asset pricing model:

Only accounts for co-movement with a market index.

②multifactor models:

To enhance the informational value of regression output.

⑵Fama-French 3-factor model:

①formula:

A.(RM-RF):CAPM single factor model

B.SMB:size premium

C.HML:value premium

②explanation:

A momentum effect could also be added to help explain excess returns.

6.Measurement of time-varying factors:

⑴Style analysis is a form of factor benchmarking where the factor exposures evolve over time.

⑵The traditional Fama-French 3-factor model can be improved by using indices that are tradable,such as the SPDR S&P value ETF (SPYV) and incorporating time-varying factors that change over time.

7.Issues with alpha measurement for nonlinear strategies:

⑴Alpha is computed using regression,which operates in a linear

framework.So there are nonlinear strategies that can make it appear that alpha exists when it actually does not.

⑵This situation is encountered when payoffs are quadratic terms or option-like terms:

This may be a significant problem for hedge funds because merger arbitrage,pairs trading,and convertible bond arbitrage strategies all have nonlinear payoffs.

8.Volatility and beta anomalies:

They both agree that stocks with higher risk,as measured by either high standard deviation or high beta,produce lower risk-adjusted returns than stocks with lower risk.

大浩浩的笔记课堂之FRM考试学习笔记合集

【正文内容】

FRM二级考试

A.Market Risk

A.市场风险

Topic 1 Estimating Market Risk Measures:An Introduction and Overview

Topic 2 Non-Parametric Approaches

Topic 3 Parametric Approaches:Extreme Value

Topic 6 Messages from the Academic Literature on Risk Management for the Trading Book

Topic 7 Some Correlation Basics:Properties,Motivation and Terminology

Topic 8 Empirical Properties of Correlation:How Do Correlation Behave in the Real World

Topic 9 Statistical Correlation Models—Can We Apply Them to Finance

Topic 10 Financial Correlation Modeling—Copula Correlations

Topic 11 Empirical Approaches to Risk Metrics and Hedging

Topic 12 The Science of Term Structure Models

Topic 13 The Shape of the Term Structure

Topic 14 The Art of Term Structure Models:Drift

Topic 15 The Art of Term Structure Models:Volatility and Distribution

Topic 16 Overnight Index Swap(OIS) Discounting

B.Credit Risk

B.信用风险

Topic 20 Default Risk:Quantitative Methodologies

Topic 21 Credit Risks and Credit Derivatives

Topic 22 Credit and Counterparty Risk

Topic 23 Spread Risk and Default Intensity Models

Topic 25 Structured Credit Risk

Topic 26 Defining Counterparty Credit Risk

Topic 27 The Evolution of Stress Testing Counterparty Exposures

Topic 28 Netting,Compression,Resets,and Termination Features

Topic 32 Default Probability,Credit Spreads and Credit Derivatives

Topic 33 Credit Value Adjustment(CVA)

Topic 35 Credit Scoring and Retail Credit Risk Management

Topic 38 Understanding the Securitization of Subprime Mortgage Credit

C.Operational Risk

C.操作风险

Topic 39 Principles for the Sound Management of Operational Risk

Topic 40 Enterprise Risk Management:Theory and Practice

Topic 41 Observations on Developments in Risk Appetite Frameworks and IT Infrastructure

Topic 42 Operational Risk Data and Governance

Topic 45 Validating Rating Models

Topic 47 Risk Capital Attribution and Risk-Adjusted Performance Measurement

Topic 48 Range of Practices and Issues in Economic Capital Framework

Topic 49 Capital Planning at Large Bank Holding Companies

Topic 50 Repurchase Agreements and Financing

Topic 51 Assessing the Quality of Risk Measures

Topic 52 Estimating Liquidity Risks

Topic 53 Liquidity and Leverage

Topic 54 The Failure Mechanics of Dealer Banks

Topic 56 Introduction of Basel Accord

Topic 58 Basel Ⅱ.5 and Fundamental Review of the Trading Book(FRTB)

D.Investment Risk

D.投资风险

Topic 62 Factors in Investment