大浩浩的笔记课堂——FRM考试学习笔记137

- 2026-04-13 13:51:25

Topic 66 VaR and Risk Budgeting in Investment Management

1.Background:

VaR is a formal-looking measure of the risk profile of a fund based-on current positions.So investors are relying more on VaR and VaR is importantbecause investors found simply measuring risk from historical measures is no longer adequate:

⑴increased globalization:

①Investments are becoming more global in nature,creating a need for risk measures that take diversification into account.

②There is a trend toward using a global custodian in the risk management of investment firms and it is easy means to the goal of centralized risk management.

⑵complexity:

Financial instruments are becoming more complex over time.

⑶dynamics of the investment industry:

Most investment portfolios are dynamic,with changing positions.

2.VaR applications to investment management:

⑴sell side vs. buy side:

characteristics | sell side (banks) | buy side (investor,such as pension fund) |

horizon | short-term(1 day,intraday) | long-term(month,quarter,years) |

turnover | rapid | slow |

leverage | high | low |

risk measures | VaR & stress tests | asset allocation & tracking error |

risk controls | position limits,VaR limits and stop-loss rules | diversification,benchmarking,and investment guidelines |

summary | 1.The horizon is short,turnover rapid,and leverage high 2.The historical measures of risk areuseless,so the VaR is particularly appropriate 3.Portfolios are highly leveraged,it is important to control their risk | 1.The horizon is much longer,positions change more slowly 2.Thus,there is a less crucial need to control the downside risk |

⑵investment process:

①A consultant provides a strategic,long-term asset-allocation study usually based on mean-variance portfolio optimization.

②The fund may delegate the actual management of funds to a stable of active managers.

③VaR-based,forward-looking risk measurement systems are essential to the investment management industry.

·特别注意!

·VaR can be used to compute better guidelines for investment companies by relying less on notions and focusing more on overall risk.

⑶hedge funds:

①They should use similar risk management systems.

②risk characteristics(more similar to "sell side"):

A.the use of leverage

B.high turnover

C.low liquidity:

It leads to problems in measuring risk because it tends to put a downward bias on volatility and correlation measures.

The risk measures are based on monthly return:

a/ correlations with other asset classes will be artificially lowered→low systematic risk

b/ volatility will be artificially lowered→low total risk

D.low transparency:

lack of transparency

3.What are the risks:

⑴absolute risk(asset risk,Rasset):

①definition:

It is the risk of a dollar loss or the total possible lossesover the horizon.

②including:

A.policy mix risk:

a/ definition:

It is the risk of a dollar loss owing the policy mix selected by the fund.(passive strategy)

b/ sources:

It is from the chooser portfolio weight.

c/ characteristic:

The most of the risk is due to the policy mix.

B.active management risk:

a/ definition:

It is the risk of a dollar loss owing to the total deviations from the policy mix.

b/ sources:

It is from the managers deviating from the chooser portfolio weight.

c/ characteristic:

The active-management VaR is rather small.

·特别注意!

·The policy-mix VaR and active-management VaR do not add up to the total-asset VaR.

⑵relative risk:

①definition:

It is the risk of a dollar loss in a fund relative to its benchmark.

②measurable:

It is measured by excess return.

③formula:

E=Rasset-Rb

④including:

A.funding risk:

a/ definition:

It is the risk that the value of assets will not be sufficient to cover the liabilities of the fund.

b/ formula:

RS=Rassets-Rliabilities*L/A

c/ characteristic:

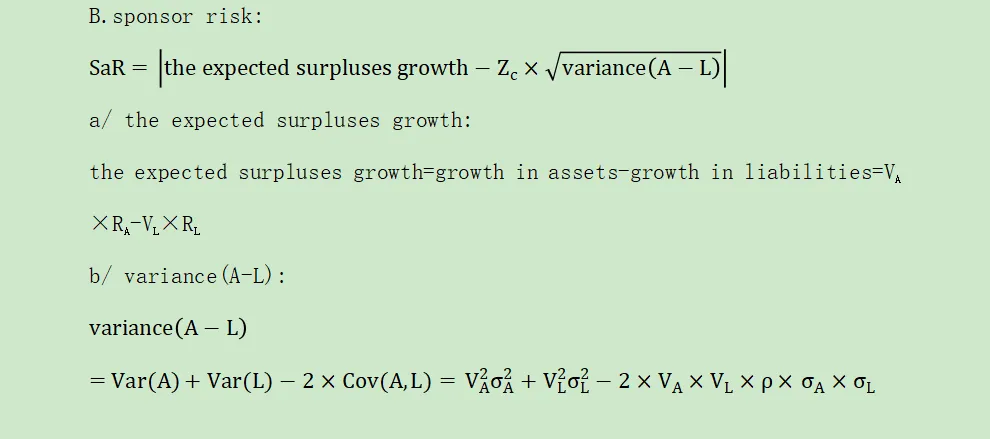

△It represents the true long term risk to the owner of the fund or plan sponsor.

△It is important for pension funds.

△In applying VaR,a manager will add the expected increase in the surplus to the surplus and subtract the VaR of the assets from it.

△The difference between the expected surplus and the portfolio VaR is the shortfall associated with the VaR.

d/ categories:

△cash-flow risk:

It is the risk of year-to-year fluctuations in contributions to the pension fund.

△economic risk:

It is the risk of variation in total economic earnings of the plan sponsor.

B.sponsor risk:

4.Using VaR to monitor and control risks:

⑴using VaR to check compliance:

VaR systems provide a central repository for all positions and allow users to catch deviations from stated policies quickly.

⑵using VaR to monitor risk:

①passive allocation:

It does not keep risk constant because the composition can charge of the indices.

②active allocation:

The explanations for the VaR jump are:

A.a manager taking more risk

B.different managers taking similar bets

C.more volatile market:

·特别注意!

·Using VaR to monitor risk is important for a larger firm with many types of managers because it can help catch rogue traders and it can detect changes in benchmark characteristics.

5.Using VaR to manage risks:

using VaR to design guidelines:

⑴VaR limits are insufficient and have blind spots.

⑵These limits can be skirted with new financial instruments.

6.Risk budgeting:

⑴introduction:

Manager establishes a risk budget for the entire portfolio and then allocates risk to individual positions based on a predetermined fund risk level.The risk budgeting process differs from market value allocation since it involves the allocation of risk.

⑵principle:

top-down allocation:

It is a top-down process that involves choosing and managing exposures to risk.

⑶methods:

①budgeting across asset classes:

A.definition:

Selecting assets whose combined VaRs are less than the total allowed.

B.objective:

To maximize return at a targeted level of risk.

C.process:

a/ first,determine the total value at risk(VaR).

b/ second,choose the optimal allocation of assets given the total risk profile.

D.advantages:

a/ Each manager is charged to earn the highest return on these risk units.

b/ It avoids micromanaging the investment process.

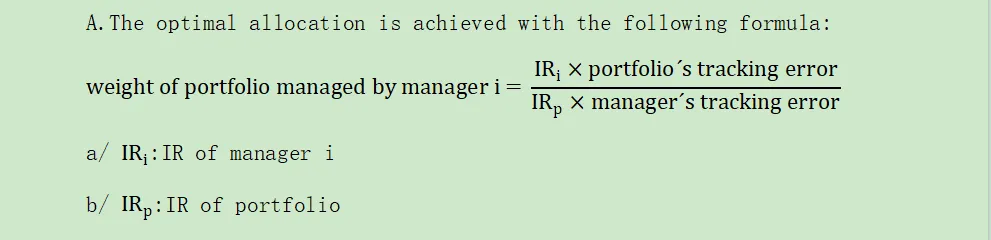

②budgeting across active managers:

A.The optimal allocation is achieved with the following formula:

B.For a given group of active managers,the weight may not sum to 1.The remainder of the weight can be allocated to the benchmark,which has no tracking error.

大浩浩的笔记课堂之FRM考试学习笔记合集

【正文内容】

FRM二级考试

A.Market Risk

A.市场风险

Topic 1 Estimating Market Risk Measures:An Introduction and Overview

Topic 2 Non-Parametric Approaches

Topic 3 Parametric Approaches:Extreme Value

Topic 6 Messages from the Academic Literature on Risk Management for the Trading Book

Topic 7 Some Correlation Basics:Properties,Motivation and Terminology

Topic 8 Empirical Properties of Correlation:How Do Correlation Behave in the Real World

Topic 9 Statistical Correlation Models—Can We Apply Them to Finance

Topic 10 Financial Correlation Modeling—Copula Correlations

Topic 11 Empirical Approaches to Risk Metrics and Hedging

Topic 12 The Science of Term Structure Models

Topic 13 The Shape of the Term Structure

Topic 14 The Art of Term Structure Models:Drift

Topic 15 The Art of Term Structure Models:Volatility and Distribution

Topic 16 Overnight Index Swap(OIS) Discounting

B.Credit Risk

B.信用风险

Topic 20 Default Risk:Quantitative Methodologies

Topic 21 Credit Risks and Credit Derivatives

Topic 22 Credit and Counterparty Risk

Topic 23 Spread Risk and Default Intensity Models

Topic 25 Structured Credit Risk

Topic 26 Defining Counterparty Credit Risk

Topic 27 The Evolution of Stress Testing Counterparty Exposures

Topic 28 Netting,Compression,Resets,and Termination Features

Topic 32 Default Probability,Credit Spreads and Credit Derivatives

Topic 33 Credit Value Adjustment(CVA)

Topic 35 Credit Scoring and Retail Credit Risk Management

Topic 38 Understanding the Securitization of Subprime Mortgage Credit

C.Operational Risk

C.操作风险

Topic 39 Principles for the Sound Management of Operational Risk

Topic 40 Enterprise Risk Management:Theory and Practice

Topic 41 Observations on Developments in Risk Appetite Frameworks and IT Infrastructure

Topic 42 Operational Risk Data and Governance

Topic 45 Validating Rating Models

Topic 47 Risk Capital Attribution and Risk-Adjusted Performance Measurement

Topic 48 Range of Practices and Issues in Economic Capital Framework

Topic 49 Capital Planning at Large Bank Holding Companies

Topic 50 Repurchase Agreements and Financing

Topic 51 Assessing the Quality of Risk Measures

Topic 52 Estimating Liquidity Risks

Topic 53 Liquidity and Leverage

Topic 54 The Failure Mechanics of Dealer Banks

Topic 56 Introduction of Basel Accord

Topic 58 Basel Ⅱ.5 and Fundamental Review of the Trading Book(FRTB)

D.Investment Risk

D.投资风险

Topic 62 Factors in Investment

Topic 63 The Low-Risk Anomaly and Alpha

Topic 65 Portfolio Risk:Analytical Methods